The FTX Fiasco is a Reminder of the Importance of Self-Custody

Crypto markets faced a meltdown last week as a black swan event, likened to the 2008 collapse of Lehman Brothers, unraveled.

As a result of the mismanagement of users’ funds, FTX, the world’s second largest crypto exchange, filed for bankruptcy on Friday due to a liquidity shortfall.

The ramifications of the failure were felt in all corners of the industry and have left investors searching for answers and rushing to withdraw their crypto from exchanges.

Elsewhere, as a result of heightened market activity, ETH turned deflationary for the first time ever.

- Cryptos crumble as investors fear contagion from FTX’s misuse of funds

- Catastrophe continues as FTX exchange is hacked

- ETH officially turns deflationary

Cryptos crumble as investors fear the contagion from FTX’s misuse of funds

The cryptocurrency market was left reeling last week from one of the worst black swan events in its history. An event that has been likened to the 2008 collapse of Lehman Brothers.

FTX led by Sam Bankman-Fried, filed for bankruptcy last week after suffering from a liquidity shortfall resulting from the misuse of customers’ digital assets.

Here are the key events as they unfolded:

- On Nov 2nd an article was published showing that Alameda Research, a trading firm associated with FTX, exhibited an unusual balance sheet; one that was heavily dependent on the success of FTX’s native token, FTT.

- On Nov 6th, the CEO of Binance, Changpeng Zhao, confirmed publicly that Binance would sell its FTT holdings. Learning from past LUNA failures was the reason provided. A back-and-forth between Bankman-Fried and Zhao ensued.

- On Nov 8th, FTX began to refuse withdrawal requests. On the same day, it was confirmed that a non-binding bailout agreement had been made between Binance and FTX.

- On Nov 9th, after only 24 hours of due diligence, Binance pulled out of the agreement. Alongside the ongoing liquidity crisis, US regulators, including the SEC and CFTC began investigating FTX for the misuse of customers’ funds.

- On Nov 10th, Alameda Research closed its doors to help the liquidity recovery. Reports of a $9.4 billion liquidity hole emerged.

- On Nov 11th, FTX filed for bankruptcy and Bankman-Fried stepped down as CEO.

The gravity of FTX’s mismanagement was eventually brought to light as both current and former FTX employees began to speak about how the company was run.

According to one employee, the entire ecosystem was run by 10 people that shared a house in the Bahamas. According to another, only 3 people controlled the code that allowed the movement of funds.

“Gary (Wang), Nishad (Singh), and Sam (Bankman-Fried) control the code, the exchange’s matching engine and funds. If they moved them around or input their own numbers, I’m not sure who would notice.”

Due to the severity of the event and the speed at which information traveled across social media platforms, the contagion of FTX quickly spread through the cryptocurrency markets.

Bitcoin fell to fresh yearly lows of $15,850, while Ethereum fell to yearly support at $1,250. After a quick, short, fall, the majority of key altcoins have managed to regain some stability.

Although painful to investors in the short-term, the collapse of FTX acutely highlighted the weakness of custodial exchanges and the need for users to remain in control of cryptocurrency private keys.

Bitcoin was created for the self-custody of wealth. It is where cryptocurrencies started; a point that is sometimes lost due to the range and variety of crypto products and services now on offer. However, it is a point that Xcoins has not forgotten.

Xcoins remains a non-custodial crypto exchange. All cryptocurrencies purchased through Xcoins remain in the control of investors at all times making Xcoins customers firmly protected against from an FTX-style collapse.

Catastrophe continues as the FTX exchange is “hacked”

One day after the FTX exchange filed for bankruptcy, admins from FTX’s telegram community group confirmed that the exchange had been “hacked” and that funds from the platform were being withdrawn maliciously.

On Saturday, Nov 12, a message was pinned by FTX U.S. General Counsel Ryne Miller, stating that “FTX has been hacked. FTX apps are malware. Delete them. Chat is open. Don’t go on the FTX site as it might download Trojans.”

Shortly after the confirmation from admins, FTX users began reporting that their wallets held in the exchange were being drained. Others that were watching transactions on-chain were tracking assets as they were being swapped to the decentralized stablecoin, DAI.

Miller quickly confirmed that all the malicious transactions were being investigated and that all remaining funds were being transferred to cold storage wallets immediately.

According to reports, over $662 million worth of users’ funds were taken mysteriously in the late hours of Friday evening. All transactions were being closely watched by members of the crypto community.

Following the event, investors began to speculate as to whether this was an attack from the inside or outside of FTX.

After the emergence that Bankman-Fried had reportedly orchestrated the disappearance of between $1-2 billion worth of customers’ funds during a transaction from FTX to Alameda Research, many fingers quickly began to point toward the ex-CEO.

According to Reuters, during a subsequent deep-dive into the platform’s accounting software, a secret ‘backdoor’ was uncovered. There is ongoing concern that a ‘backdoor’ may have been programmed into the platform. A backdoor that allows someone to execute commands to alter financial records without notifying anyone.

Both FTX and Alameda Research were run from the Bahamas, where Sam Bankman-Fried is still believed to be. Both the Bahamian government and US authority investigations are still ongoing.

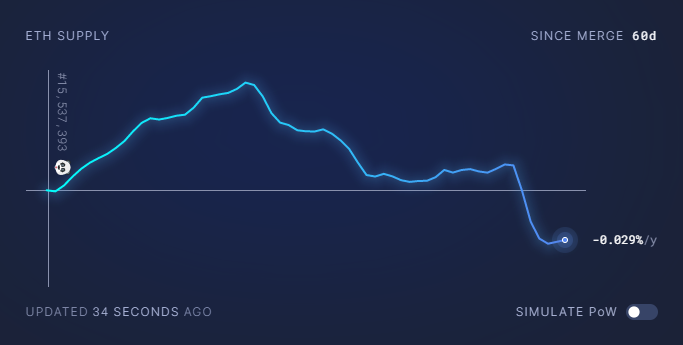

ETH officially turns deflationary

The native coin of Ethereum, ETH, has turned deflationary for the first time since the blockchain’s Merge.

According to data collected by ultrasound.money, on Friday, the coin’s net issuance dropped to -0.029%, a figure that indicates that the world’s leading smart contract blockchain is now burning more ETH than it is minting.

From an inflation rate of 3.5%, the Merge reduced Ethereum’s inflation rate to near zero by swapping Ethereum miners for validators. A swap that greatly reduced the number of ETH that are minted each day.

While many had speculated that the swap from miners to validators would result in an instant deflationary mechanic, it has taken 60 days since the Ethereum Merge for that to become a reality. It appears the increase in network usage, potentially created by recent market volatility, could be the reason.

As a certain fraction of ETH is burned during each transaction, increased transactions lead to an increase in the amount of ETH burned.

According to Etherscan, the blockchain burned 5000 ETH on Wednesday, which is the highest daily figure since June; a day that corresponded with heightened market volatility stemming from the collapse of the FTX ecosystem.

With the first hint of deflationary mechanics, many are now speculating if Ethereum can one day outperform Bitcoin.

The supply of ETH since the Ethereum Merge.

To stay up to date on all things crypto, like Xcoins on Facebook, and follow us on Twitter, Instagram, and LinkedIn.