Impending Wallet Rules Are on Hold but Yellen Signals Stricter Crypto Regulations to Follow

President Biden’s administration has frozen all new regulatory proposals left open by the Trump administration pending review. The new administration issued the order shortly after the 46th President was inaugurated.

The freeze includes the FinCEN cryptocurrency wallet rules introduced by the former Treasury Secretary, Steve Mnuchin. The rules, which were proposed towards the end of last year, would require cryptocurrency exchanges to verify the ownership of “non-hosted” cryptocurrency wallets before allowing users to withdraw their holdings.

The reaction so far

At the time, the proposals met a harsh response from the cryptocurrency community. Many pointed to the stringent verification requirements already in place. Users are already required to upload identity verification documents in order to be able to withdraw large sums.

Adding more checks to this process would only lengthen and complicate the process with unnecessary steps. Prominent commentator and partner at Blockchain Capital, Ben Davenport, wrote an open letter to FinCEN, outlining a number of reasons why the new rule would only serve to stall innovation in the industry.

These critics welcome the new administration’s freeze as the first step towards listening to the industry. However, they are also cognizant of the fact that the new administration has a mixed bag of cryptocurrency supporters and critics.

Harsher regulation to follow

Enter Janet Yellen. Yellen who is set to become the new secretary of the Treasury Department, commented on Bitcoin during her confirmation hearing in the U.S. Senate. In the comments, Yellen suggested “curtailing” cryptocurrencies such as Bitcoin (BTC) in an effort to prevent money-laundering. This, Yellen believes, is the main use of the top-cryptocurrency.

The comments come as the President of the European Central Bank, Christine Lagarde, also said she thought cryptocurrencies such as Bitcoin are linked to “totally-reprehensible money-laundering activity”.

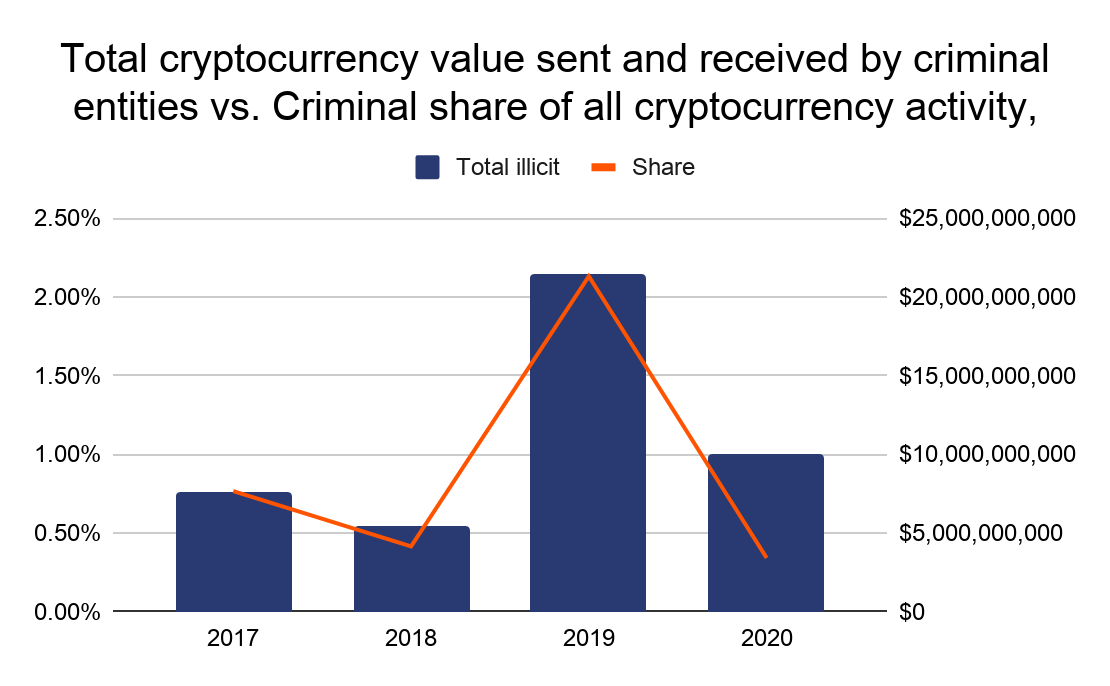

Despite these comments, data produced by leading cryptocurrency analytics firm Chainanalysis, suggest that the involvement of cryptocurrencies in criminal activity fell by over 75% in 2020, compared to 2019. ”In 2019, criminal activity represented 2.1% of all cryptocurrency transaction volume, or roughly $21.4 billion worth of transfers. In 2020, the criminal share of all cryptocurrency activity fell to just 0.34%, or $10.0 billion in transaction volume. One reason the percentage of criminal activity fell is because overall economic activity nearly tripled between 2019 and 2020” says the new Chainanalysis report.

Source: Chainanalysis

Nevertheless, the beliefs of arguably the most influential individual in the US economy likely means tougher regulation will follow the freeze. We have already seen the proposal of the STABLE Act which aims to safeguard the financially vulnerable from unregulated stablecoin issuers. Yellen will likely become a supporter of that Act and try to make the FinCEN rules as expansive.

However, the new administration isn’t all anti-cryptocurrency. The administration’s pick for chair of the Securities and Exchange Commission (SEC), Gary Gensler, is a former MIT Blockchain professor. In the past, Gensler has called Bitcoin the “modern form of gold”.

His position on the SEC, which is likely to be involved in any cryptocurrency rule-making, means at least the government will have some understanding of the intricacies of the industry.

Moreover, if cryptocurrencies are to become mainstream long-term, combatting any associated criminal activity is a must.

To stay up to date on all things crypto, like Xcoins on Facebook, follow us on Twitter and enter your email address at the bottom of the page to subscribe.